The Chancellor announced his Spring 2024 Budget, no doubt with one eye on the upcoming General Election. He did not announce any major policy changes, leading to speculation that there may be a further mini-Budget before voting day. Time will tell if any significant tax changes are announced in the coming months, but Alec James meanwhile provides a summary of the key points from Jeremy Hunt’s latest address at the dispatch box

Tax rates and bands

As in in the last few Budgets, income tax rates and lower tax brackets remain unchanged for 2024-25.

The exception, of course, being that, from 6 April 2024, the additional rate of income tax now takes effect with earnings over £125,140 – previously £150,000.

It had already been announced in the January 2024 Scottish Budget that the additional rate of tax would be increased from 45% to 48%.

The personal allowance, which was last increased from 6 April 2021, remains unchanged.

Many have seen that while there has been no increase in the tax rates, the freezing of the bands and personal allowances at a time when inflation has been running far higher than it has in the past means taxpayers are subsequently worse off.

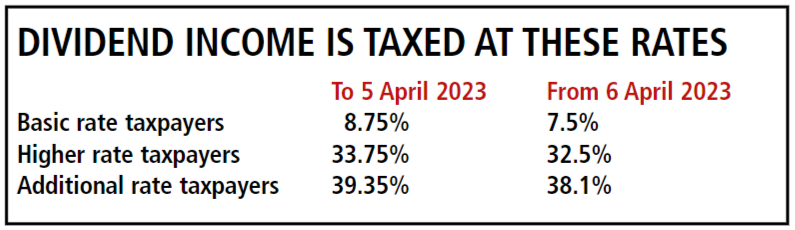

Beware of triggering hidden taxes

Company Cars and The NHS Fleet Scheme

Many doctors will have heard of company cars or the NHS fleet scheme. Both are very similar.

The difference is that company car costs are a deduction against your company profits, whereas the NHS fleet scheme costs are a deduction against your pensionable and taxable income from your NHS employment income.

To cover the personal use of the vehicles, the taxpayer with use of the vehicle is required to pay tax on the benefit-in-kind value of using the car.

This is calculated by taking the list price of the vehicle multiplied by a percentage which is based on the CO2 emissions of a vehicle and the fuel the vehicles use.

These schemes became popular when HM Revenue and Customs (HMRC) reduced the benefit-in-kind rates on fully electric vehicles to 0% in April 2020. They are currently 2% of the list price of the car.

This results in very minimal tax being due on the benefit in kind but significant tax savings for the deduction of the costs of the car.

As you approach retirement, and even before, you will likely need to consider what will happen to your private practice when you retire. Can you sell it? Who could buy it?

Alec James, Partner, looks at ways your private practice could be sold, ways of improving the business viability for someone purchasing the business and alternative options to selling

2023 was a significant year heralding change for the country’s finances – and yours. In this year before the next general election, there were key changes around pensions and other measures that benefit doctors – but some changes that have not.

Partner, Ian Tongue, highlights what doctors with a private practice business need to know for the year ahead

Doctors are facing many changes around the tax system and rates – and these may have a significant impact on your private practice business. Some of these measures have already been introduced and others are planned for the near future.

BASIS PERIOD REFORM

Basis period reform applies to sole traders and partnerships where their financial accounts are drawn up to a date that is not coterminous with the fiscal year-end, which is 5 April – or 31 March for many in practice.

These year-end dates have often arisen from the commencement of the business or, for older businesses, when the self-assessment tax system was introduced.

Legislation has now been introduced so that you have to report your profits to 31 March/5 April 2024, which may be a change to your usual year-end.

You do not officially have to change the date of your accounts, but it is expected that most businesses will, unless you are expecting significant differences between accounting years, in which case some planning may be required.

The impact of the change is that it can accelerate income tax due on the profits, as it unwinds the timing difference for the disclosure of earnings.

This creates overlap profit, or in other words, you have used the same profits twice on the first period of 1 July 2010 to 5 April 2011.

This can be a benefit if profits are rising, as it builds in a timing difference that you are effectively paying the tax on profits later.

Over the life of your practice, this would naturally unwind with usually a higher tax liability in the final year, often well after the business has, in fact, ceased.

The basis period reforms basically unwind the timing difference to align the disclosure for tax to the tax year-end. In doing so, the first period that was included twice is deducted from the longer period.

Value Added Tax is a levy applied to most products and services. It is a complex tax, but for many businesses it is part of the day-to-day finances. VAT is charged on invoices and recovered on certain costs incurred.

There are special provisions within the VAT legislation specific to medical services, but reviewing and evidencing that those exemptions apply is extremely important. Alec James gives some wise advice.

Generally speaking, VAT is not on the radar of many doctors. The reason is that there is an exemption which covers the majority of your work in the private sector.

There is detailed HM Revenue and Customs (HMRC) guidance regarding VAT for medics, referred to as VAT notice 701/57.

Fundamentally, where your income meets the following two requirements, the income is deemed to be exempt from VAT and therefore your business has no VAT obligations:

1 The services are within the profession in which you are registered to practice;

2The primary purpose of the services is the protection, maintenance or restoration of the health of the person concerned.

As registered doctors providing medical care to patients, your private practice income would usually pass these two tests and therefore is exempt from VAT.

This means you are not required to charge the current VAT rate of 20% on your invoices.

Where an income stream does not meet the two requirements for VAT exemption, you need to consider your VAT position, because the income will be considered to be a ‘VAT-able supply’ – or ‘standard-rated’ as it is formally known.

Opportunities to work in groups are now on the increase for more consultants. Richard Norbury gives tips on the various structures you need to consider

With the NHS’s current challenges, the focus is on cutting waiting list times – but many consultants are understandably anxious about performing additional work and being paid extra salary under PAYE.

They are obviously concerned for a variety of reasons, including:

* High tax rates;

* Loss of certain childcare benefits;

* The potential tapering of the annual allowance causing additional pension tax charges.

Now NHS trusts are becoming more innovative to try and reduce their waiting list times and are under significant pressure to do so.

And that means consultants may have opportunities to group together.

This could be in a variety of formats with different levels of commitment, starting from a loose/cost-sharing arrangement to a more formal legal structure such as a company or limited liability partnership (LLP).

It is important to establish the common goals and objectives of the group as early as possible, because this will, no doubt, have an impact on the decisions made, including which tax structure you choose.

Consultants who are new to their posts may find they are offered the opportunity to join existing arrangements. They will have varying commitment levels to such groups, from being very involved in the management to effectively subcontracting.

UK inflation rates have recently seen a large rise in response to a variety of factors.

Understandably, many doctors are now thinking about how savings and investments keep pace with inflation. Interest and gains on investments often cause tax charges.

Partner Richard Norbury looks at practical and tax issues to consider with common investment areas

Due to high income tax and potential tax charges on pension growth, many doctors trading as limited companies will not be withdrawing all the available funds from the company.

If you are in this position and the money is building up to sizeable amounts, then these sums can be considered for investing.

2023 is set to be a testing time for independent practitioners’ finances following Chancellor Jeremy Hunt’s Autumn Statement. Partner, Richard Norbury, sets out what is waiting in the wings and suggests some useful action points for you to take now to limit the damage.

There has been a mixed response to the Chancellor’s changes, but many professional commentators highlight that further tax measures and spending cuts may be announced after the 2024 General Election, regardless of which party comes to power.

The term ‘fiscal drag’ has been used by professional commentators to highlight that although basic and higher rates of tax have remained unchanged, it will, in a period of inflation, bring more individuals into paying higher rates of tax.

Annual allowance – don’t you just hate the restrictions? Partner, Alec James gives an update on the tax charges on your pensions.

Many readers may not be aware that when the pension savings annual allowance was first introduced in April 2006, the allowance was £215,000 rising in successive years to £255,000.

This meant that considering the annual allowance position was rarely an issue for doctors. However, when the markets took a downturn in 2008, it was seen by successive governments as a mechanism to generate more tax by reductions in the allowance. The allowance is now normally £40,000, but can decrease down to £4,000 if tapering is applied.

Extreme busyness goes with the territory of clinicians when they are occupied with their NHS commitments, private practice and other roles. As their careers progress, it is likely their tax affairs will become more complex and it is easy to miss some vital dates. That can be financially costly as well as increasing the chance of a HM Revenue and Customs (HMRC) inquiry.

Partner, Richard Norbury covers some of the more common tax deadlines you will face during your career

Individuals

Most readers will surely be familiar with the tax return deadline of 31 January. In recent years, this has been extended to 28 February due to Covid.

But it is expected that the usual 31 January deadline will now be enforced in future. The majority of consultants and GPs will be required to prepare a tax return by this date.

Here are few of the most common reasons why you might need to submit a personal tax return: