Doctors are facing many changes around the tax system and rates – and these may have a significant impact on your private practice business. Some of these measures have already been introduced and others are planned for the near future.

BASIS PERIOD REFORM

Basis period reform applies to sole traders and partnerships where their financial accounts are drawn up to a date that is not coterminous with the fiscal year-end, which is 5 April – or 31 March for many in practice.

These year-end dates have often arisen from the commencement of the business or, for older businesses, when the self-assessment tax system was introduced.

Legislation has now been introduced so that you have to report your profits to 31 March/5 April 2024, which may be a change to your usual year-end.

You do not officially have to change the date of your accounts, but it is expected that most businesses will, unless you are expecting significant differences between accounting years, in which case some planning may be required.

The impact of the change is that it can accelerate income tax due on the profits, as it unwinds the timing difference for the disclosure of earnings.

This creates overlap profit, or in other words, you have used the same profits twice on the first period of 1 July 2010 to 5 April 2011.

This can be a benefit if profits are rising, as it builds in a timing difference that you are effectively paying the tax on profits later.

Over the life of your practice, this would naturally unwind with usually a higher tax liability in the final year, often well after the business has, in fact, ceased.

The basis period reforms basically unwind the timing difference to align the disclosure for tax to the tax year-end. In doing so, the first period that was included twice is deducted from the longer period.

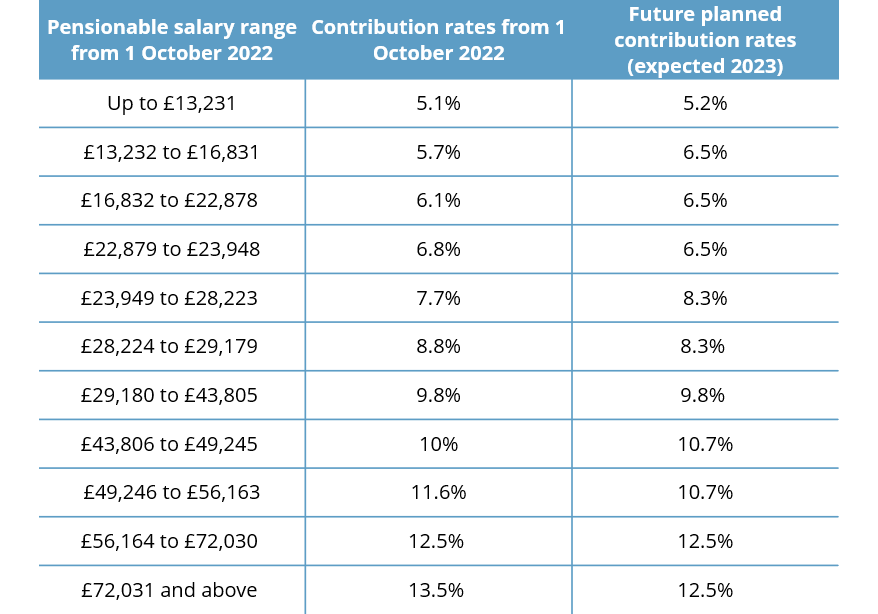

All members of the NHS pension scheme pay a percentage of their pensionable pay towards the scheme. From 1st October 2022, the amount you pay for your pension will change and further changes are planned in 2023. For many of you, this may result in a lower percentage paid in pension contributions.

Many of you that had been transferred into the 2015 NHS Pension Scheme are aware of the 2015 Remedy also known as the McCloud remedy whereby you will be returned to the 1995 or 2008 scheme (if you had opted in the past to join the 2008 scheme) up to 31 March 2022 after which future pensionable service for all will be in the 2015 scheme.

The Scottish Public Pension Agency (SPPA) has dedicated webpages detailing the background of who is affected and what course action will be undertaken. By 1 October 2023 they anticipate to have implemented all the necessary changes. Click here to view the site.

This will be a Herculean task and hopefully free of errors or omissions.

To safeguard against any errors or omissions we would suggest the Annual Benefit Statement that is available each year and for previous years are accessed, downloaded and saved.

These statements might be removed/revised from March 2022 onwards, if not earlier.

New Annual Benefit Statements will be prepared and by retaining old copies it at least allows you to check they have the correct pensionable service history, added years (where applicable) and pensionable salary at the end of each year of service.

If you have suffered an Annual Allowance tax charge the new Annual Benefit Statements allow one to check or at least estimate any revised growth and whether a refund of tax is due.

The main contents of the Budget, like most ministerial announcements these days, were leaked well in advance of yesterday’s announcement by the Chancellor, Rishi Sunak. He continues with his well-publicised aim to keep to the government manifesto promises and set the UK back on track to reduce its indebtedness arising from the pandemic.

Below is a summary of the main points that we understand will impact you.

The Coronavirus Job Retention Scheme - Extended

The Furlough Scheme has been extended until 30 September 2021 and the level of grant available to employers under the scheme will remain the same until 30 June 2021.

From July 2021, the Government contribution will reduce to 70% dropping down to 60% in August 2021.

To be eligible for the grant employers must continue to pay their furloughed employees at least 80% of their wages, up to a cap of £2,500 per month for the time they spend on furlough.

Income Tax Thresholds

The personal allowance will increase to £12,570 and remain frozen at this level through to the end of 2026. The basic rate tax threshold will increase to £37,700 and will also remain frozen at this level through to 2026.

Different rates and allowances apply to Scotland and can be found here

On the 4 February 2021 the government announced its response to the consultation in respect of public pensions. This is important as it includes your NHS Pension and sets out how the government proposes to remedy the discrimination found by the courts by transferring certain scheme members to the ‘reformed’ 2015 NHS Pension Scheme from the ‘legacy’ scheme, the 1995/2008 NHS Pension Scheme.

The response and proposed remedy are extensive but below we provide a summary of the key points.

- Dependent on age many of you will have transferred over to the ‘reformed’, 2015 NHS Pension Scheme, on 1 April 2015 or later under transitional arrangements. You will now be transferred back to the ‘legacy’ scheme, if you were in the 1995 scheme you will revert to the 1995 pension scheme rules and members of the 2008 scheme will revert to the 2008 NHS scheme rules.

- In the run up to retirement and intended from 2023, two Annual Benefit Statements will be produced showing the above to assist you in deciding when to retire.

- You will remain in the ‘legacy’ scheme up until 31 March 2022 after which all future service will be transferred over to the ‘reformed’, 2015 NHS Pension Scheme. This will also apply to members who had not been transferred to the ‘reformed’, 2015 NHS Pension Scheme and but for this consultation would have remained in the ‘legacy’, 1995/2008 NHS Pension Scheme.

- At retirement you will be offered what is known as a Deferred Choice Underpin (DCU). What this means is that two calculations of your NHS Pension benefits will be provided. These will be as members of the ‘legacy’ scheme, 1995/2008 NHS Pensions for the period 1 April 2015 through to 31 March 2022. The second choice as members of the ‘reformed’, 2015 Scheme from 1 April 2015 through to 31 March 2022. These dates will vary if you were a transitional member.

- Annual Allowance charges paid either personally or by way of Scheme Pay Elections will have to be revisited to determine if additional tax or a refund is due. For any additional tax payable, limits on how far the Revenue can go back are provided which is not to exceed four years but there are no time limits on refunds or alterations to Scheme Pay Elections already made.

- Should at the date of retirement you decide to choose to return to the ‘reformed’ scheme, (2015 NHS Pension) for the period 1 April 2015 through to 31 March 2022, there will be very high pension growth in your final year which under normal circumstances would result in a substantial annual allowance charge. However, under the proposals it appears to be that no tax will be payable under these circumstances.

Action Points

- For many of you no action is required at the moment as the necessary legislative changes are needed to be put in place. However, since it will not be until 2023 possibly at the earliest that the NHS Pensions will be able to provide the two Annual Benefit Statements and as a consequence revised Annual Allowance Statements, many of you may wish some indication if a refund or additional tax could arise as a result of these changes and at least provide a method to check the accuracy of what will be produced by the NHS Pensions in the future.

As a firm we have the system in place to undertake these calculations to provide an indication of any refunds or additional tax due and for these to be used to check future statements produced by NHS Pensions. Many doctors may be eligible to reclaim thousands of pounds in Annual Allowance tax previously paid.

This service is available to consultants & GPs both in England & Wales administered by NHS Pensions and for consultants in Scotland administered by the Scottish Public Pensions Agency (SPPA).

- If you have recently retired and had been a member of the ‘reformed’ 2015 NHS pension in the run up to retirement you will be entitled to your benefits being recalculated should you decide as a member of the ‘legacy’ , 1995/2008 NHS Pension Scheme. This is important if you took early retirement on the grounds of ill health.

- Some of you made the choice to become deferred members of the NHS Pension Scheme, the majority being GPs in England & Wales and some consultants in Scotland by way of special arrangements in 2019/20 to mitigate Annual Allowance tax charges. There is scope to return to the scheme for the periods that you deferred but this will be dealt with on an individual basis.